By: Steven Abernathy

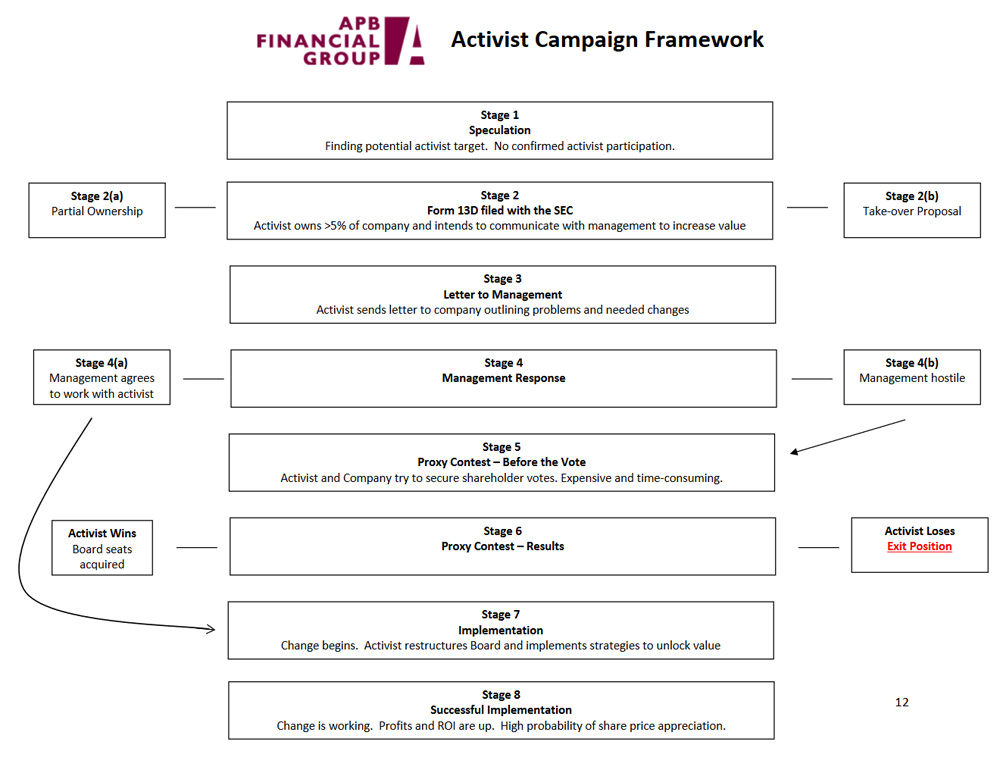

Every investment has risks. Shareholder Activism, introduced in Part 1 here is no different. However, as in most investments, its inherent risks can be isolated and controlled. Below is the step-by-step process of an activism campaign along with the risk associated of each of the eight stages of development:

No investor is right about their investment thesis 100% of the time, however, the fundamental framework for investing alongside activists is relatively transparent and easy to monitor as filings and reporting happens publicly. There are 5 variables most intelligent investors require before investing with any activist:

(a) Ensure true value is significantly higher than current price;

(b) Understand the clear path toward value creation;

(c) Know there’s a high probability for change to take place;

(d) Ensure activist investing a significant amount of their own money as lead investor;

(e) Be assured the activist has a solid track record of success.

While every investment in a public security involves risks, investing in significantly undervalued assets, with documented changes outlined by some of the best investors in the world is a great place to start your investment process. The financial risks associated with investing alongside activists are similar to most other equity type investments, yet, there are significant differences which make activism particularly attractive:

Less downside – an investment in a security which is the subject of an activist campaign often has the characteristics of a value-investment. It generally holds less downside as hard assets, which could easily be sold, support the “true value”. Equally often, a value-investment may own a significant amount of cash and marketable securities. Most of the time, the share price is lower than it has been over the last few years indicating general and widespread shareholder disapproval.

More upside – it seems counter-intuitive for an investment to have less risk and more reward. The secret sauce is: (a) event-related change and (b) probability of the outcome. When the company is damaged the market believes the odds are higher than normal it will not be fixed—therefore current price is low relative to true value. And when it’s fixed, there is typically significant upside as the target company goes from “dog” to “darling.”

When the market believes a company is broken and either cannot or will not be fixed, an opportunity exists. Activists are confident their initiatives will change the company for the better and they put a significant amount of their own money, and reputation, behind their investment in the target company. This usually triggers share price appreciation. The possibility of a superior return is a function of the low current share price relative to the company’s true value. The larger the difference between current price and true value, the greater the upside potential.

Event-related share price movement lowers investment correlation. The success of investing with activists largely depends on events and changes they initiate such as: improved operational efficiency, a sale of underutilized assets, closing businesses which lose money, or the intelligent addition of assets generally leading to a corporate turnaround. If such changes create value and narrow the gap between current price and true value, there will be change(s) surrounding the target company. An increase in share ownership, offer to buy the whole company or management agreeing to adopt some—or all—of the activist’s suggestions, are highly likely to bring about change.

The financial rewards for being involved in an activist target may be significant. An activist rarely embraces the amount of work involved in this long, sometimes contentious process of corporate improvement, if there isn’t something substantial to be gained. Studies show that independent of market movement, on average, changes causing improvements in operating the business often translate into significant share-price appreciation which clearly outpaces the market’s returns.

Many things may thwart a campaign—all of the mistakes possible with any investment can happen. Risks include the activist overvaluing the company, overestimating product demand and underestimating product obsolescence. Lack of management depth, and implementing the wrong operating strategy, also offer risks.

Turning around a company, rolling up similar companies, or selling divisions which seem to be destroying value all involve risk. While these certainties exist, intelligent investors should never forget that shareholder activism risks are often lower than general market risk, as the activist typically buys the asset closer to its “tangible book-value.”

What needs to happen for a campaign to work?

Per the breakdown of the eight stages above, change is necessary. However, at any stage the campaign can fall apart. When an activist gets a significant amount of shareholders supporting their cause, the odds shift in their favor, thus increasing the probability of success.

In many cases, the activist does not need to pursue a costly, time consuming, and highly emotional proxy contest (shareholder vote) as management understands they’ll lose a vote. Once management understands shareholders truly want change to protect and grow their investment, they often settle with the activists, embrace change, and try to keep their jobs by going along with the activists.

Take, for example, Insperity (NSP). Activist Starboard Value took their initial position of a 13.2% stake in January 2015 announced in their 13D filing. Working in tandem with Stadium Capital, the activists initiated several changes. Starboard Value also nominated two individuals for election to Insperity’s board last month based on an agreement made last year to takeover three board seats. Detailed recommendations included: exploring a sale or initiating share repurchases and reducing overhead costs, such as selling the company’s private planes and itself! .

At present, after following all of the activist’s recommendations, the company is poised to continue unlocking shareholder value. Given the sheer number of small and mid-size businesses which could benefit from its services, Insperity could be a market leader—they have a great deal of room to grow.

The benefits of activism are obvious and could possibly alter the future of the consulting firm model. Given that activists invest their own money in a company before they turn it around, they align with all other shareholders from the get-go. Activists could be offered a percentage of the firm’s profits realized from their efforts. This model of compensation is significantly better aligned with shareholder value creation than one in which management writes incredibly large checks to pay for advice lacking any shareholder alignment.

Shareholder activism also offers a level of diversification as it allows participation in the equity markets, yet follows an appreciation path dominated by company-specific events, less related to the general market movements. It is allows intelligent investors to simplify their investment process by standing on the shoulders of the “smart money” with a vested interest in success. The herculean effort of turning around a struggling company may demand the application of new technology, the result of which may be fewer employees. But fewer employees are better than no employees.

Steven Abernathy is the co-founder and Chairman of The Abernathy Group II Family Office. Expert in shareholder rights. Applied the art of value investing to the Medical and IT sectors at Cowen & Co. Contributor to publications including Forbes, Barron’s, Wall Street Journal, Huffington Post, Private Air, The American Association of Individual Investors, Family Wealth Report, Medical Economics, Physicians Money Digest, Chiropractic Economics, Medscape, Practice Link, Practical Dermatology, Physicians Practice, Dental Practice Management, Buyside Magazine, The Bottom Line and more. Featured in Money Magazine.

Click here to view this article in the original magazine publication