Footnotes will be a monthly publication which follows our “First Friday” webinar presentations each month. The goal of the Footnotes publication is to summarize our “First Friday” presentation’s most important data points, which will make it easier for The Abernathy Group Family Office members to make intelligent decisions based on facts and data – as opposed to potentially conflicted opinions – from the mainstream media.

Click here to view the corresponding First Friday Video

Commentary from the May “First-Friday” meeting:

May’s “First Friday” meeting focused on Identifying the categories of companies, public and private, most likely to become the winners and losers in the Artificial Intelligence world which is unfolding in front of us in real time.

While May’s “First Friday” meeting focused on Artificial Intelligence’s technological leap forward, it reminded everyone watching that significant changes in technological advances usher in changes which are unplanned. They will be, mostly positive. However, there could be negative changes also. The one certainty is change. Since the evolution of the steam engine, electricity, transportation, the integrated circuit, creation of mobile computers and the internet, certain categories of the U.S. and global population have been advantaged – and some have been disadvantaged. And quite often those disadvantaged at first, become the advantaged over time.

On balance, technological changes have created a world which is magnitudes better off in almost every important variable affecting human lifespans, safety, poverty levels, and decision-making. However, it is incredibly important for all investors to remember Schumpeter’s economic principal of “Creative Destruction.” A short summary reminds us – as innovations are introduced and adopted, they create efficiencies and changes leading to a better world. Yet, these innovations may destroy less desired segments of our economy, demanding that mankind change. And at times change is disruptive. This is why identifying the winners and losers is a topic worthy of consideration.

As a short reminder to each Family Office member, The Abernathy Group Family Office has now had 12+ “First Friday” webinars. All of them are available on our website and “YouTube” Channel if you would like to go back and see how we have interpreted the economic signals, while doing our best to cancel the noise over the last year plus. Our goal: to help our Family Office members save time and make intelligent decisions by ignoring information with little predictive power and focusing on data with the highest probability of telling us what is to come.

Today, we are going to discuss the most potentially disruptive change our world has embraced since the invention of the internet.

As we discussed 2 months ago, while we do not believe Artificial Intelligence is as disruptive or transformative as the internet, we do believe it is an incredible step forward for mankind and will both increase efficiencies in our personal and global business world, and allow us to make better, more informed decisions in every facet of our lives.

Let me take a moment and explain the logic behind this statement.

Artificial Intelligence, at our current stage of development, is really what we should be calling advanced “machine learning.” Machine learning reads and remembers everything it is trained on. Then, it leverages an enormous amount of computing power, with newly developed Large Language Models (LLM’s) to order relevant data into a response and in a language we can understand. With access to the enormity of data available on the internet, Artificial Intelligence will soon offer an understandable answer to almost any question you can pose. However, keep in mind, sometimes it’s wrong.

I am not trying to denigrate this technology in any way, yet I do want to call it what it is.

Our current iteration of Artificial Intelligence takes all of the information it has been trained on, and produces answers based on that information. It is still in its adolescent stages… so we must be diligent in our questions, and always demand references backing the information Artificial Intelligence uses to answer the question (at least until we get the bugs out).

Time and experience will get the majority of the bugs out. Eventually we will continue to increase the dataset Artificial Intelligence LLM’s are trained on giving us access to all information ever recorded.

Artificial Intelligence is NOT sentient. It is not conscious. It does not create… rather it gathers data, orders it, and gives it back in unique ways – in the form of an answer, or a spreadsheet or code it is asked to provide.

The first order effects of this technology will be an increase in efficiency. It will allow every user with access to a networked computer to be smarter, while increasing productivity – allowing humans to do more with less. It may allow humans to be more creative as answers to questions will take less time to find, leaving us more time to be creative.

Slide 2

Since this is a developing technology and its moving at warp speed, we want to simplify our categorization of how we think about its evolution.

As time evolves more categorizations will become clear. Innovation will create more categories, each with winners and losers.

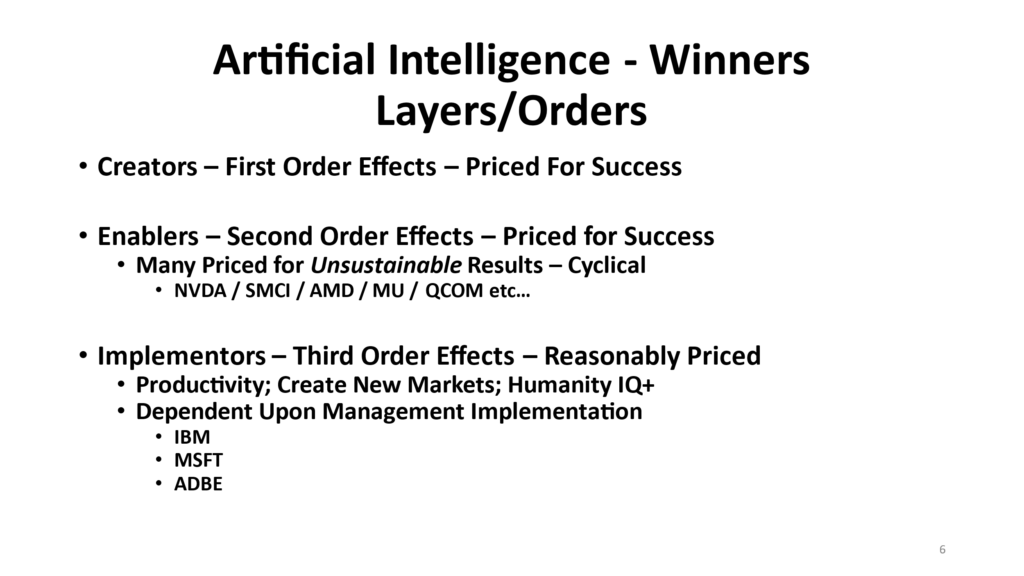

So, from the top down, one reasonable way to order this technology is in 3 categories.

- Creators – those who invented Artificial Intelligence.

- Enablers – supplying the tools allowing Artificial Intelligence to work.

- Implementers – those using Artificial Intelligence – beneficiaries.

Slide 3

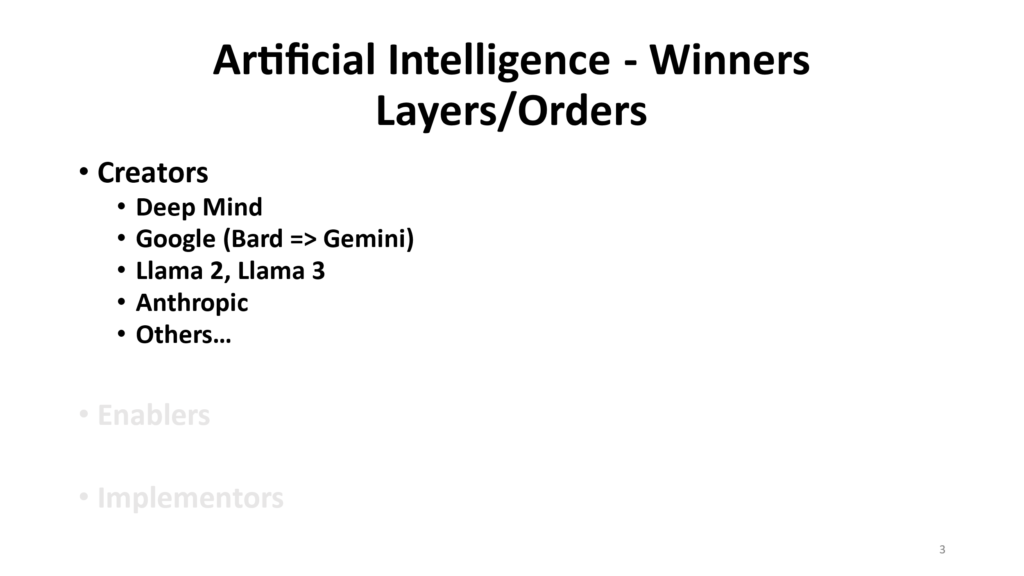

Creators – for example are now well known, and many of the creators are on their 3rd, 4th, or 5th, iteration of Artificial Intelligence’s maturation.

The “Creators” represent the Deep Minds and Googles of the world. (One brief Google-search will give you a long list of creators.) *Note – most of the creators are either private, part of a larger company or, if publicly traded, have priced in a future associated with near perfection.

Slide 4

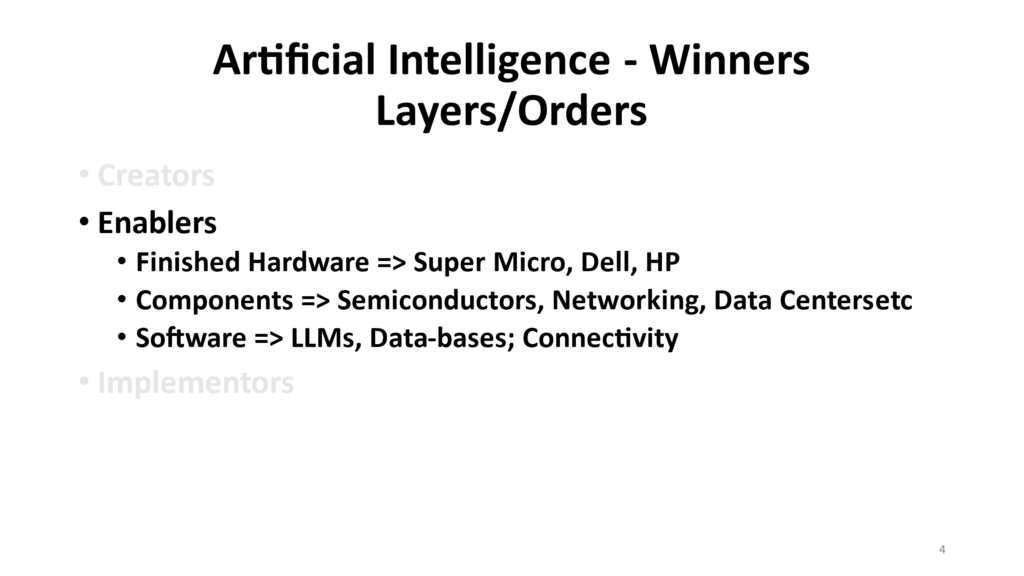

The second order of Artificial Intelligence belongs to a category we can call the “Enablers.”

These are the companies supplying the equipment necessary to enable the technology – or to actually implement the technology. This category of Artificial Intelligence is equivalent to those supplying the picks and shovels for the gold rush in the 1800’s.

The high-level categories are Hardware, the components that go into the hardware, and the software which allows the hardware to communicate data and information we can use to make decisions.

Slide 5

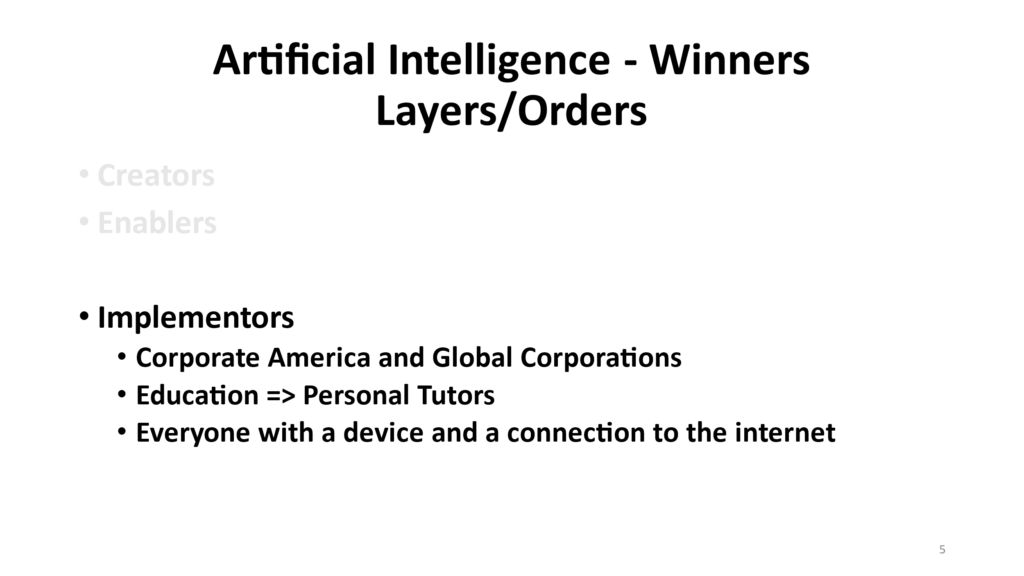

Lastly, we can group the 3rd order set of beneficiaries as the “Implementors”, as these are the users of the Artificial Intelligence to produce products, goods and services consumers use daily.

And as you will see, this is where the benefits of this technology will be realized and leveraged most abundantly.

So, considering the broad categories – who are the broad-brush winners? And who are broad brush losers?

And importantly for the focus of this summarized overview, where are the opportunities for intelligent investors?

Let’s take a look at each of the categories through the lens of current valuation and current mania…

Slide 6

The creators were initially largely private and were well-funded over a decade ago.

While the creator category has expanded a bit since then, most of the creators are fully priced, or are still largely private, or are a division of a public company which adopted the technology privately, years ago.

In short, the “Creators” are representative of the “First Order” affects and are fully priced or are unavailable to public investors at this time.

Next, let’s consider the “Enablers.”

The capital markets have taken the opportunity to price in expectations of growth exceeding the boundaries of reality for most companies in the “Enabler” category.

Intelligent investors must remember, once the new infrastructure is built, mass adoption occurs, along with a typical mania. Then, as mass adoption is satisfied, growth will slow, prices will become competitive, which will reduce profit margins. Next, earnings will normalize and become cyclical (based on technological adoption cycles) as it has for the last 150 years, each time a new technology thundered onto the scene.

Our view: The “Enabler” category is speculatively priced. Many have priced in a future which is unlikely to be obtainable, while others are fully priced leaving little/no room for true investors to earn a realistic return. We are not saying the companies which comprise the “Enabler” category are worthless. These are high quality companies with bright futures ahead over the “adoption” phase of Artificial Intelligence. What we are saying from a professional investor’s perspective, most current valuations reflect a measure of success associated with a future which will be very difficult to achieve.

Our advice is to avoid the “Enabler” category unless prices offer investors a lower entry point, thus a higher probability of an acceptable return on investment.

The 3rd order Effects are the most interesting and the most diverse. Corporate America will adopt this technology in varying amounts and with varying speed.

It is reasonable to assume those who successfully adopt this technology will weave it into the everyday corporate activity. These companies will experience the affects sooner and most notably.

Some examples of the early movers, most likely to realize the benefits are companies like Microsoft, IBM, and Adobe – among many others including the pharmaceutical industry which will benefit from discovering molecule activity faster and with less costs. The biotechnology and pharmaceutical industry will use Artificial Intelligence to accelerate clinical trials and likely reduce the cost of isolating therapies which will increase life-spans and quality of life. The energy industry will also benefit by identifying energy deposits faster and will find ways to capture carbon more efficiently. The software industry will benefit as code writing will become faster and more accurate, which will lead to the need for fewer programmers, thus lowering costs… the list of beneficiaries is long and inclusive yet will largely depend upon management’s adoption and implementation of Artificial Intelligence. The creation of beneficiaries will create disruption, some easy to identify, some only identifiable in hindsight.

So, who are the identifiable losers at this early stage of development?

Slide 7

It is too early to tell exactly who this technology will affect most significantly… yet those most easily identified are the non-specialized employee segments of the workforce.

One seemingly obvious example – clearly within the sites of Artificial Intelligence is the educational system in America.

As many of you know – I have been anticipating education changing since the 1990’s. I will clearly admit to being early, however, Artificial Intelligence offers no chance for the cost of education to remain stagnant. Educational costs will plumet while opportunities skyrocket. Everyone with access to a computer – and initiative – will become smarter, as almost all information ever created will be readily available; ready to answer any, and every question you can pose.

Eventually, each company will have a resident (Artificial Intelligence) authority on all of their internal data fostering more effective decision-making.

Each person will have a personal tutor available in every topic you can imagine.

The shortest summary is that the early “losers” can be readily identified. Employment in these industries, in general, will become pressured initially, and over time, it is quite likely that other categories of industry will be created just as it has for the last 150 years.

Many categories of industry included in “losers” will be replaced by digital solutions. However, it will take some time to get to this point. Nevertheless, it seems clear that unless you are specialized, Artificial Intelligence will increase productivity and usher in Schumpeter’s theory of “Creative Destruction.”

(On the bright side: soon, each of us calling “customer service” with almost any question, will be able to talk to an intelligent entity, more likely to solve our problem, in a language or accent we understand (not to mention shorter “hold” times 😊).

To summarize this topic:

The “first” and “second” order categories of corporate America have already largely priced in the reality to come, and in many instances – overpriced the change which is most likely. Current valuation leaves little opportunity for investors in these categories of Artificial Intelligence adoption. In some instances, current fairy-tale valuations will end in tears, with many investors asking themselves why they paid “X” price for “X” company?

Our take is that the most likely beneficiaries which are priced reasonably from this point forward are the third order beneficiaries; those companies who are able to harness and implement Artificial Intelligence most effectively.

Let’s stop here and check in to take the questions I believe we have on the docket so far along with any new questions which may have come in during this discussion.

Marissa, I think I saw some questions coming in… if so, can you let us know what they are?

Question 1: For those of us interested in looking for value in the “enabler” category, what innovations may be early enough in the adoption process to offer some upside?

For most people, Artificial Intelligence will be running in the cloud. Over the next year the Artificial Intelligence algorithms will migrate closer to the edge of the network so recall times are faster. Eventually your PC may be able to run some of the Artificial Intelligence queries on your computer itself, requiring massive amounts of memory and computing power.

This evolution will take time. At some point it will require you to purchase a new PC which is optimized for Artificial Intelligence, creating an upgrade cycle. This may evolve similar to the gaming upgrade cycle, as many who used their computer for gaming, were required to upgrade their computer to include “gaming chips” because the games themselves used so much bandwidth and memory, normal processors could not handle gaming demands. This ushered in a period where “gamers” (and bitcoin miners) needed specialized computers. Artificial Intelligence may evolve similarly. New computers over the next several years will be able to depend less on the “cloud” for responses to Artificial Intelligence related questions. This will make all responses faster. In short, the “edge” network is still being built and the winners/losers are still to be named.

My advice is to wait for a year or so before you upgrade your computer (and your phone). The PC will be reborn again. What we call our cell phone today, could become our personal assistant in a future which is nearer than many think. The combination of cybersecurity demands along with new infrastructure available, will, at some point, demand that you upgrade your computer, your phone, and maybe our behavior.

One strong note of caution: The spending taking place in the Artificial Intelligence buildout is estimated to be over $750 billion in 2024, and maybe that again in 2025. This spending must create profits – or – there will be a sharp downturn in every category of company currently shouting to the world that they are adopting Artificial Intelligence company-wide. In short, intelligent investors will watch profits. Over the next 12 months or sooner, if profit generation based on either revenue increases or cost reductions does not show up, the current euphoria will unwind.

I hope that is helpful – and as always, if not, call me and we can discuss it offline.

Marissa, is there another question or two?

Marissa – What does the U.S. Federal Reserve’s decision this week mean to equity markets over the next year or so?

U.S. growth is currently being supported by legacy liquidity. This liquidity is from the incredible amount of stimulus infused during the pandemic and shortly thereafter.

Excess liquidity increased consumer’s balance sheet. It allowed some to reduce debt, and others to refinance their debt at the lowest levels in 30 years. This created a spending-spree which overwhelmed supply availability – which resulted in our most recent bout of inflation.

Federal budget deficits continue to run at 7% of GDP or more, amidst a healthy economy.

In short, our belief is that inflation will remain stickier than most realize. This will force the U.S. Federal Reserve to keep rates higher than they would like.

Eventually, something in our economy will break, and the U.S. Federal Reserve will lower rates to fix our economy and stop the downturn.

We do not believe the U.S. Federal Reserve will allow the economy to go through a downturn because of the amount of debt the U.S. has accumulated over the last 20 years.

Our current period is eerily reminiscent of the late 1960s.

During the 1960s, unemployment was at 4%, and the labor market was tight. Inflation was about the same then, as it is today, between 3-4%.

That wonderful economy was created by very low interest rates and significant spending by our U.S. government in the years prior. (Sound familiar?)

What followed this period of a Goldilocks economy, was the 1970s inflation. And I don’t need to tell most of you about the economic downturn this created. What I do want to mention is that the 1970’s downturn took place with less than $500 billion in debt… and today we have over $34 trillion in debt…

What is clear to us is that the tailwinds which ushered in the earnings growth over the last 20+ years are not going to be with us over the next 20 years.

Interest rate decreases will not provide tailwinds which increase corporate earnings.

Lower corporate taxes will not provide the tailwinds which increase corporate earnings.

Increased levels of debt will be unlikely to offer the leverage which created the tailwinds of the last 20 years. Why? corporate debt today cost 7-10% or more. This exceeds most of corporate America’s profit margins today. So, borrowing money at 8% and producing profit margins of 6% or below ensures every dollar of debt reduces earnings. Corporate America’s game of borrowing money to increase earnings is over. Tailwinds are gone.

(and by the way, our U.S. government likely earns less than 1% on every dollar it borrows at 5% interest rates today – so how do you think that is going to end…)

If inflation remains more persistent than the U.S. Federal Reserve believes, earnings will suffer. Corporate profit margins will decline from their current historically high levels and will not satisfy the market’s current expectations for 10%+ earnings growth in 2024, and 12%+ earnings growth in 2025.

While I do not know what our most likely future will be, the combination of our $34T of debt, combined with planned overspending of 1.5 trillion (plus) during the next year, ensures the U.S. Federal Reserve must lower rates.

Why?

Financing $1 – 2 trillion in deficits each year is possible with U.S. 10-year bonds paying 1% per year. However, with 10-year rates at 5%, debt levels are unsustainable, and will eventually end with a less than desirable outcome for most.

Our belief is that the U.S. Federal Reserve’s help will work during the next downturn. However, slower growth will mean more frequent recessions. Debt repayments will for the U.S. to spend an unsustainable amount of GDP on interest payments alone.

At some point, in a future nearer than the capital markets have priced in, the world will force the U.S. Federal Reserve to pay more for the debt they are issuing. When that moment comes, incredibly difficult decisions will have to be made. Higher taxes, fewer services, are likely to be in our future. Maybe Artificial Intelligence can tell us how to solve this problem…😊