By: Vito J. Racanelli

Download a PDF version of this article

The third-quarter rise was small enough to let a majority of hedge funds best the S&P 500

The rather pedestrian 2.2% rise in the Standard & Poor’s 500 index in the third quarter this year was a big letdown for most investors, coming as it did after the benchmark’s 14.9% second-quarter moon shot. Hedge fund managers, however, aren’t complaining. Unlike mutual funds, hedge funds can sell stocks short, as well as buy them, so they tend to do better when the broad market wanes. Short sellers borrow shares then sell them in the hopes of making a profit by buying the share later at a lower price.

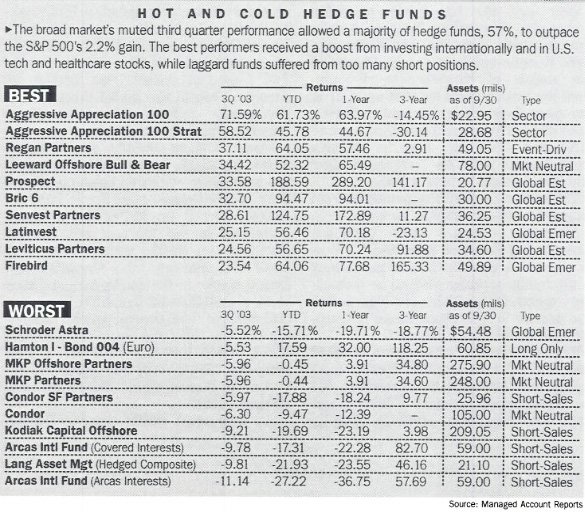

And the market’s third-quarter advance was small enough to allow a majority of hedge funds to best the S&P in the July-September period. Some 57% of hedge funds tracked by the CISDM Database, listed monthly in the industry newsletter MarHedge, topped the S&P in the quarter. That’s a healthy jump from the measly 20% or so that beat the S&P’s huge April-May surge from its March lows.

Hedge funds are investment pools for heavyweight investors, like institutions and high net worth individuals, that are generally unregulated, although that might change soon.

Several key factors aided the quarterly showing, says Greg Newton, the president of MarHedge. Obviously, the fewer short positions held, the fatter the return, but many funds made hay outside the U.S., particularly those holding shares in red-hot emerging markets like Russia or Brazil, as well as developed markets like Japan and Hong Kong, he adds.

For example, the benchmark for many funds that invest abroad—the MSCI EAFE (Europe, Australasia, Far East) Index—rose a healthy 8% during the third quarter, so you’ll find several funds with global mandates among the top ten in the tables nearby, and just one, a bond fund, in the bottom ten.

And in many cases, he adds, the plunge in the dollar just turbocharged performance for managers who held foreign shares in local currencies, many of which rose against the greenback.

“Now that Treasury Secretary John Snow [essentially] has pronounced that the dollar is free to fall,” currency gains likely will continue to boost funds investing outside the U.S., Newton contends.

In other cases, the best performers did well with the help of soaring technology stocks or certain health-care issues. “A life sciences fund or a tech fund may have had a position that just exploded” and pushed the whole fund solidly higher, Newton avers.

At the bottom of the list you’ll find the aggressive shorts, or funds in which the majority of investments are shorts most of the time. “It’s a simple truism,” Newton adds, that when the market is up solidly then hedge funds will struggle because many have short positions that will bite them in a rally, such as we’ve seen this year. It’s worth noting, however, that some 395 of the 699 funds surveyed beat the market in the most recently ended three-month stretch, and that 573, or 70%, had positive returns in an up quarter, he adds.

Of course, the further you track the data back into the bear market, the better the hedge funds do. For example, only about a third of funds were able to surpass the S&P’s 22.2% increase in the 12 months ended Sept. 30, but going back 36 months, a period that essentially covers the brunt of the bear market, then a whopping 99% of funds outdid the 30.7% drop in the S&P 500.

Several long-term investments in health care and technology “really started to blossom for us” in the third quarter, says Steven Abernathy, principal at The Abernathy Group, which runs the top two finishers, Aggressive Appreciation 100 fund, up 71.6%, and the Aggressive Appreciation 100 Strategy fund, up 58.5%. (The latter is a combination of the 100 fund plus separately managed individual accounts.)

Over half the 100 fund’s quarterly return was provided by Netgear, a company in which Abernathy had invested in 2000; it came public last July. Shares of this maker of wireless-network-equipment for small businesses shot up to 21 at one point from an initial public offering price of 14. They’ve since slipped back to 17.80, and Abernathy says he remains “comfortable” with his Netgear holding over the next six to nine months.

The rest of the fund’s return came from diverse health-care stocks, he adds.

Abernathy operates these portfolios through “collaborative investing,” a process in which those invited to put money in the funds—wealthy medical or technology experts, for example—are expected to also provide insight about issues concerning their respective industries.

Regan Partners, which came in third with a 37.1% return, didn’t benefit from foreign exposure or rising currencies, but its performance received a nice boost from two long-term holdings, Per-Se Technologies, a health-care transaction processor, and Century Business Services, a tax and accounting firm. Shares of both jumped sharply, helping to buoy what is a small and mid-cap fund “with very few names,” says portfolio manager Basil Regan. He likes troubled companies that have good balance sheets and offer turnaround potential, and adds he’s still happy with both firms’ 2004-2005 outlook.

Brendan Kyne, who runs the Leeward Offshore Bull & Bear fund, likes to play the traditional negative correlation between Canadian natural resources stocks and U.S. consumer and financial companies. Investments in Canada’s DVD-maker Cinram International and America’s Urban Outfitters, which he has since sold off, helped fuel a 34.4% quarterly return. The Canadian dollar’s rise against its American cousin also added three to four percentage points gain, and Kyne remains bullish on the loonie.

Other winners include the Prospect Fund, up 33.6%, which invests in small-cap technology stocks and also boasts the best year-to-date return, a gain of 188.6%; Bric 6, up 32.7%, and a repeat performer in the top ten; and Senvest Partners, up 28.6%, which focuses on small and mid-cap U.S., Canadian, and Israeli stocks in the health-care and tech sectors and thereby benefited from several positive third-quarter trends. Rounding out the top finishers is the Firebird Fund, which has done well for a long time—up 1,000% over ten years—by investing in Russia, where stocks are near all-time highs.

As a general caveat, readers should consider that the performance tables suffer somewhat from a survivorship bias and from the fact that there are significantly more hedge funds that don’t report results and thus aren’t included. Additionally, the size of the fund does matter. “It’s easier for smaller funds to move in and out of markets,” says Newton. That’s a reason to single out Vega Select Opportunities, he says, which finished 12th in the quarter and has nearly $1 billion in assets, dwarfing most of its peers.

And what of the cellar dwellers? Dead last is Arcas International. It’s a repeat offender, but that doesn’t much bother Dave Hammond, a principal at Derivative Consulting Group, its parent, because it’s a 100% short, quantitative-based fund designed to be used as a “blending agent” by other large fund managers who have a long bias, in order to offset some risk.

Penultimate place goes to Lang Asset Management Hedged Composite, a more traditional fund run by a make-no-bones-about-it bear, Robert Lang. “The market is still ridiculously overvalued,” he grouses about the furious rally this year from March lows. Many metrics, like price-to-earnings and price-to-sales ratios, investor complacency levels, all indicate this remains an overpriced market, contends an unbowed Lang, who isn’t about to change his style.

Don’t be too hard on the bottom of the pack. The Lang fund, for example, as well as seven of the other bottom ten hedge funds, have trounced the S&P 500 by a wide margin in the three years ended Sept. 30, and investing is still a long-term game.

Click here to view this article in the original magazine publication